Every Tuesday afternoon we publish a collection of topics and give our expert opinion about the Equity Markets.

In recent years, passive investing has transformed the landscape of the global stock market. Investors have been flocking to index funds and exchange-traded funds (ETFs) due to their lower costs, broad diversification, and simplicity. This shift has led to a growing concentration of capital in passive strategies, leaving many to question the future of active managers. Are we approaching a tipping point where passive funds dominate to such an extent that active managers become obsolete, or is there still a place for active management in a market where passive investing controls the majority of assets? ABSI this week will explore the active passive balance in stock markets.

It is important to appreciate that passive investing has experienced explosive growth over the past two decades. According to Morningstar, passive funds accounted for nearly 55% of all U.S. equity fund assets as of 2023, a dramatic rise from just 12% in 1998. This surge is driven largely by the consistent underperformance of many active managers relative to their benchmarks, coupled with the high fees associated with active management. For many investors, the prospect of tracking an index like the S&P 500 at a fraction of the cost has been an irresistible proposition.

Source: The Economist

This dominance has created a stock market where trillions of dollars are controlled by passive strategies that are agnostic to individual company fundamentals. Instead, passive funds mechanically buy stocks according to their market capitalisation or other predefined criteria.

Based on the current trajectory, could we approach a future whereby the world’s largest companies are exclusively owned by passive investors and the shares effectively don’t trade?

Yes, it is a possibility, but no it isn’t probable.

In a scenario whereby passive funds eventually control such a large portion of the market that liquidity dries up in many stocks, this could result in fewer trading opportunities for active managers and a vicious cycle where investors pull more money out of active strategies due to their inability to outperform. The role of active managers might shift to specialised areas such as small-cap stocks, emerging markets, or alternative asset classes where passive funds are less prevalent.

However, what is more likely to occur is the growth of passive funds eventually creating significant market inefficiencies, with stock prices becoming increasingly disconnected from fundamentals. In this case, active managers could make a comeback by exploiting these inefficiencies, especially in less liquid or less followed sectors.

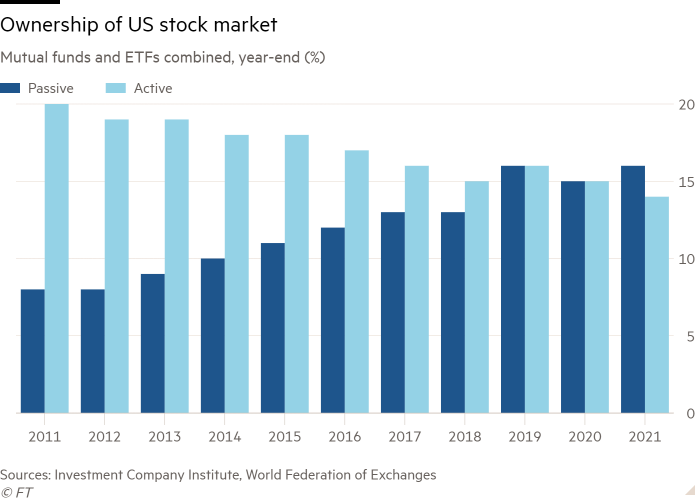

So when would that tipping point occur for passive funds?

Source: Financial Times

That is very difficult to discern but could come quicker than expected if the growth trajectories of passive funds continue. In 2010, passive funds owned ~10% of the Nasdaq 100 and 8% of the S&P 500. By 2020, this had increased to ~30% and 21.2% for the Nasdaq 100 and S&P 500 respectively, overtaking active ownership in the process.

The current market environment is incredibly difficult for active managers given the increasing passive ownership. Anecdotally, in a recent discussion I had with a large Australia-based global fund manager, they lamented finding great opportunities but are unable to follow through due to a lack of liquidity to acquire a meaningful position in a stock with a market capitalisation in the many multiples of billions. There is no doubt that passive ownership plays a major role in this issue.

Outside of liquidity, other issues active managers are contending with include shrinking alpha opportunities due to passive strategies' indiscriminate buying, greater price volatility, wider price spreads, trade crowding, market concentration, and lapses in corporate governance due to lack of engagement from passive managers.

Active stock picking is a difficult profession and the rise of passive investment options compounds the difficulty. As passive strategies continue to capture market share, active managers will need to adapt by focusing on areas where they can still add value, likely in the form of small-cap, emerging market, and other specialised strategies. Although the future may be more challenging for active management, it is unlikely that passive funds will completely eliminate the need for active strategies, especially in less liquid or more complex markets. The key for active managers will be to evolve and find new ways to generate alpha in a world increasingly shaped by passive capital flows.

Introducing BPC Wealth Management

BPC Wealth Management is dedicated to shaping resilient investment portfolios, empowering you to achieve and sustain your financial aspirations. While the foundation of your portfolio focuses on long-term investments, through BPC, clients will be offered opportunities in equities trading and equity capital markets. This aspect is highly customised, allowing asset flexibility. Discover how our proactive and client-focused approach can help you achieve your financial aspirations by booking your discovery call with James Whelan.

We offer value-rich content to our BPC community of subscribers. If you're interested in the stock market, you will enjoy our exclusive mailing lists focused on all aspects of the market.

To receive our exclusive E-Newsletter, subscribe to 'As Barclay Sees It' now.

{kind=link}